Understanding Zero-Based Budgeting for Families

Zero-based budgeting (ZBB) is a financial planning method where every dollar of your income is assigned a specific purpose. Unlike traditional budgeting methods that use previous spending habits to forecast future expenses, zero-based budgeting starts from scratch each month, requiring you to justify all expenses.

For families, this approach can foster greater financial awareness and control, as it encourages participation and communication among family members about financial priorities and goals.

The Core Principles of Zero-Based Budgeting

Zero-based budgeting involves creating a new budget from a 'zero base' for each period. This method demands detailed tracking and justification for each expense, which ensures that resources are directed toward the most impactful activities. Let's delve into the core principles:

- Income Allocation: Begin by listing all sources of income, including salaries, side hustles, and any government benefits.

- Expense Justification: For every dollar spent, there must be a clear justification. This involves categorizing expenditures into essential (e.g., rent, utilities) and discretionary spending (e.g., dining out, entertainment).

- Monthly Evaluation: At the end of each month, evaluate your spending to ensure it aligns with your family's financial goals. Adjustments should be made in subsequent months to improve resource allocation.

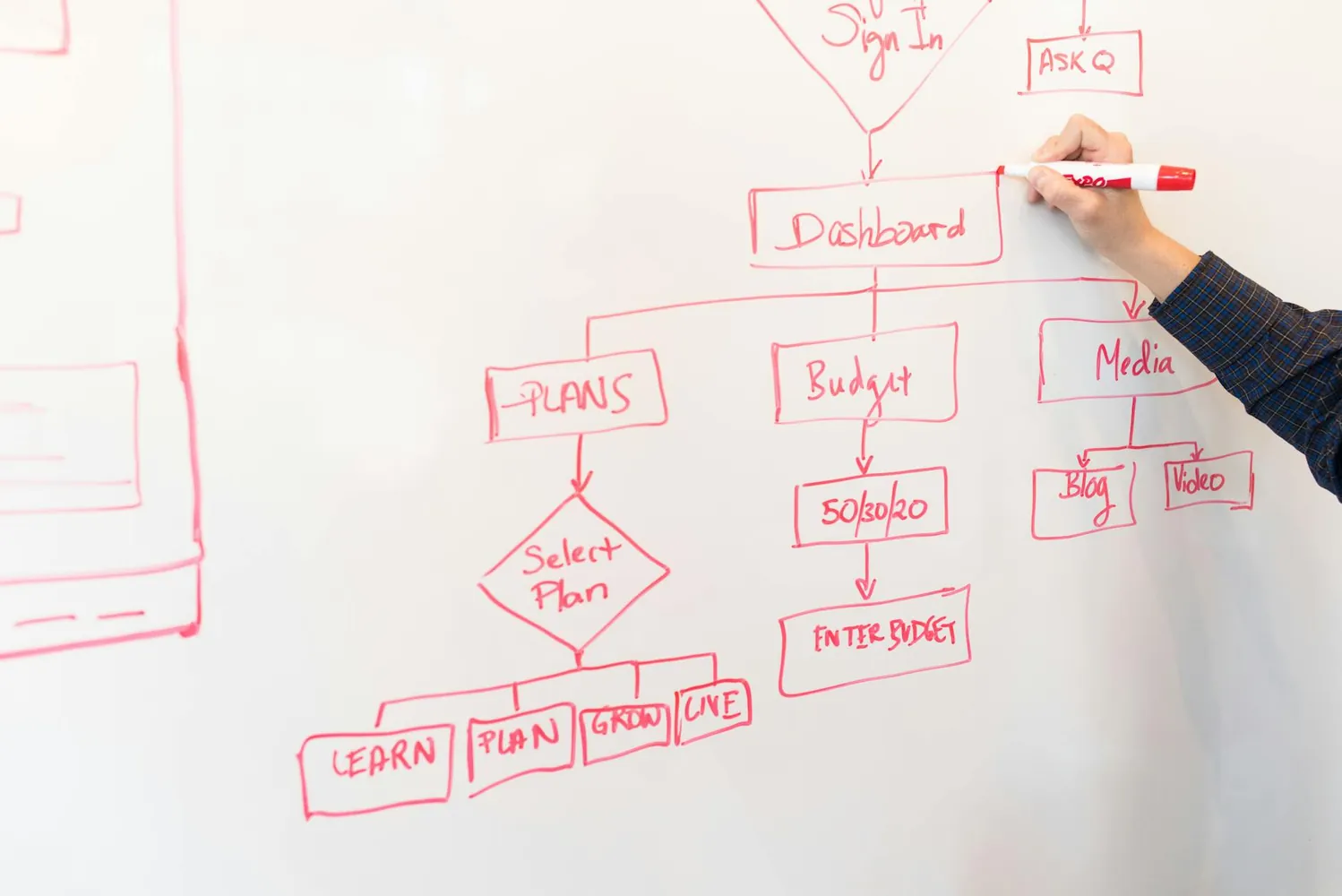

Setting Up a Family Zero-Based Budget

Step 1: Gather Income Information

Begin by calculating your total household income. Include all reliable streams of revenue:

- Salaries and wages

- Rental income

- Freelance or gig economy earnings

- Child support or alimony

This comprehensive list gives you a clear picture of the funds available for allocation.

Step 2: Identify and List Expenses

Categorize your expenses into fixed and variable categories. Fixed expenses are those that remain constant each month, such as:

- Mortgage or rent payments

- Insurance premiums

- Car payments

Variable expenses fluctuate and may include groceries, utilities, and transportation costs. For families, it's crucial to allocate funds toward children's education, health care, and extracurricular activities.

Step 3: Prioritize Essential Spending

Essential expenses should always take priority in your zero-based budget. These are non-negotiable items that ensure the well-being and functioning of your household. Once essentials are covered, you can consider discretionary spending.

Step 4: Allocate Funds to Savings and Debt Repayment

An essential aspect of zero-based budgeting is planning for savings and debt repayment. Allocate a portion of your income to an emergency fund, retirement savings, or college funds. Similarly, prioritize paying off high-interest debts such as credit card balances.

A Case Study: The Rodriguez Family

Consider the Rodriguez family, who successfully implemented zero-based budgeting to transform their financial situation. With three children and two working parents, they found themselves struggling with mounting credit card debt and little savings.

Their Process:

- The Rodriguezes listed all their income sources, which totaled $6,500 per month.

- They outlined fixed expenses: $1,800 for rent, $400 for utilities, $350 for insurance.

- The variable expenses included $700 for groceries, $200 for dining out, $150 for entertainment.

By rigorously applying zero-based budgeting principles, they identified areas to cut back on discretionary spending. They reduced dining out expenses by cooking more meals at home and adjusted their entertainment budget by exploring free community events. This reallocation allowed them to increase their monthly debt repayments from $300 to $500.

Tips for Successful Family Zero-Based Budgeting

The key to effective zero-based budgeting lies in organization and discipline. Here are some practical tips to help your family succeed:

- Involve the Whole Family: Encourage open discussions about financial goals with all family members. Children can participate by setting their own saving goals or helping with grocery planning.

- Use Budgeting Tools: Leverage apps such as You Need A Budget (YNAB) or Mint for tracking expenses and automating calculations.

- Regular Reviews: Set a monthly meeting to review budget performance and make necessary adjustments based on actual spending.

The Benefits of Zero-Based Budgeting for Families

This approach not only promotes fiscal responsibility but also fosters a deeper understanding of where money goes each month. As families become more mindful of their spending habits, they can better align their financial decisions with long-term goals such as buying a home or saving for college tuition.

The Rodriguez family discovered that through zero-based budgeting, they achieved improved financial stability. Within one year, they paid off significant portions of their debt while increasing their savings cushion from $1,000 to $5,000.

Conclusion: Empower Your Family’s Financial Future

Implementing a zero-based budget tailored for families requires commitment and collaboration but ultimately leads to enhanced financial control and security. By ensuring every dollar is accounted for, families can move closer to achieving their financial dreams without unnecessary stress or uncertainty.